The Next Phase of Global EV Growth Will Be Regional, Affordable, and Multi-Speed

How electrification, rising Chinese automakers, fuel-price volatility, and regional market realities are reshaping the global automotive industry through 2030

A Global Market at Scale, but Entering a Different Phase

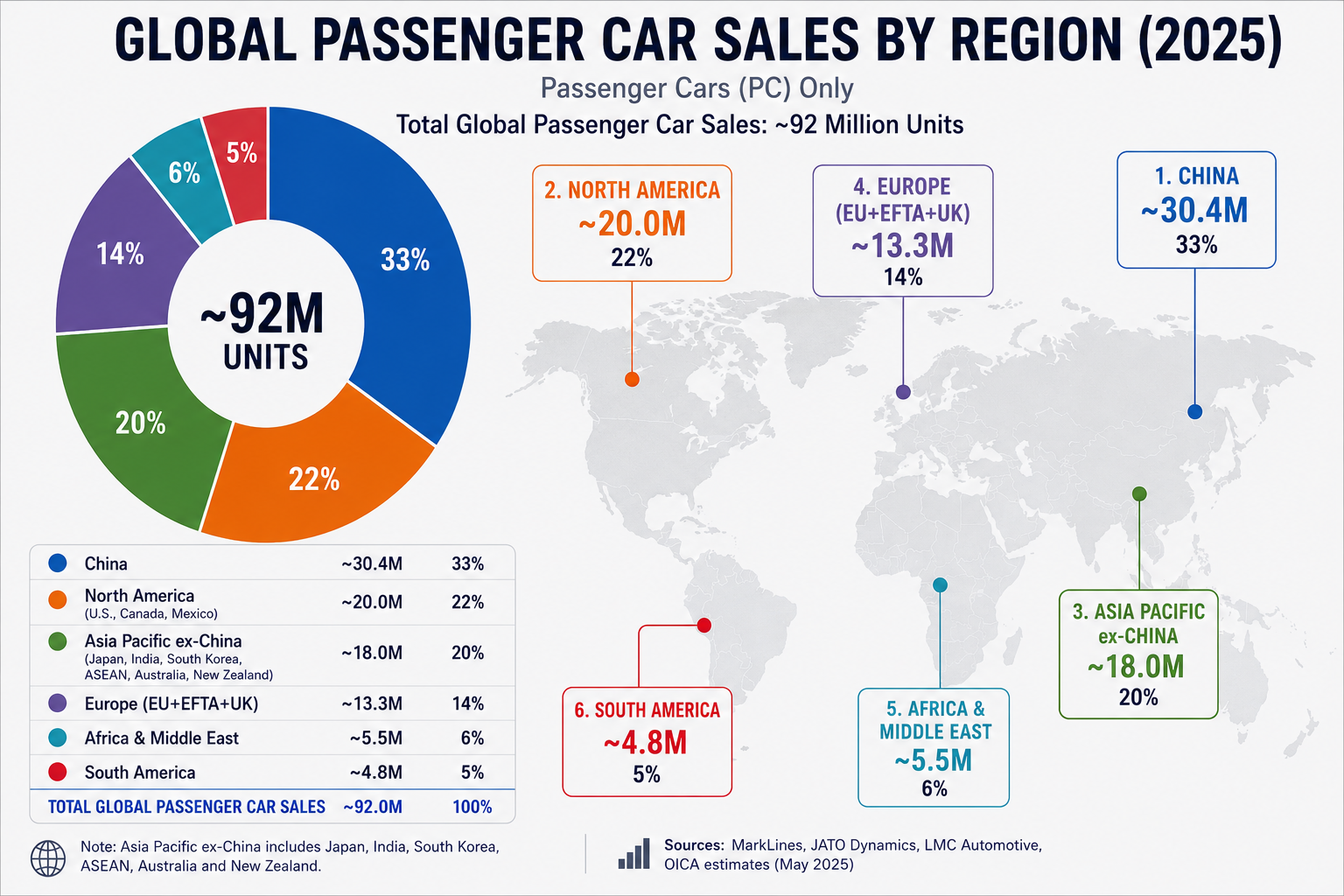

Global passenger vehicle sales in 2025 reached ~92 million units, ~96 million if you include commercial vehicles.

After several years of pandemic disruption, semiconductor shortages, logistics bottlenecks, and supply-chain instability, the automotive industry largely returned to near pre-pandemic production and sales levels through 2024 and 2025.

However, the broader operating environment has not fully normalized as new geopolitical tensions, energy-market volatility, tariff escalation, and renewed concerns around semiconductor localization, battery supply chains, and critical mineral access suggest that a new phase of industrial and supply-chain pressure may already be forming.

The majority of incremental global passenger vehicle growth 2025 came from electrified vehicles, while internal combustion engine (ICE) vehicle sales remained largely flat, or declined, across many major markets.

However, the transition toward electrification is no longer unfolding at a single global speed or through a universal model. Instead, EV adoption is diverging across regions based on affordability, infrastructure readiness, energy economics, government policy, and consumer practicality.

The result is a global automotive industry evolving into a multi-speed NEV era, shaped as much by economics and infrastructure realities as by technology itself.

Despite strong electrification momentum, adoption rates remain highly uneven across regions, specifically charging infrastructure limitations, electricity-grid reliability, affordability constraints, tariff barriers, and the gradual reduction of EV subsidies continue to slow mass-market adoption across many developing and price-sensitive markets.

1. Global Car Sales in 2025 Driven by NEVs

The industry grew by 3-4 million units, ICE vehicles still dominated with over 70%, but NEVs are now closing in on 25% of total sales and growing fast.

Of those:

- Battery electric vehicles (BEVs): ~16 million units

- Plug-in hybrid electric vehicles (PHEVs): ~6 million units

- Total NEV sales (EV + PHEV): ~22 million units

- NEV share of global passenger vehicle sales: ~24%

Perhaps most significantly, nearly one in four passenger vehicles sold globally in 2025 was either a battery electric vehicle (BEV) or a plug-in hybrid (PHEV), up from one in five in 2024. Unlike previous automotive growth cycles driven primarily by internal combustion vehicles, most incremental global passenger vehicle growth in 2025, estimated at 3–4 million units, came from NEV sales, while demand for traditional ICE vehicles remained largely flat across many major markets.

NEVs accounted for nearly 1 in 4 global passenger vehicle sales in 2025, driving virtually all net industry growth while ICE vehicle demand largely stagnated.

The Center of Gravity Continues Shifting Toward Asia

China remained the world’s largest automotive market in 2025 with ~30.4 million passenger vehicle sales, representing roughly 33% of total global volume.

China alone accounted for two-thirds of global NEV sales in 2025, while Southeast Asia emerged as one of the world’s fastest-growing electrification regions as affordable EVs and plug-in hybrids expanded rapidly across ASEAN markets.

Combined, China and Southeast Asia accounted for over 6 out of every 10 NEVs sold globally in 2025, reinforcing Asia’s growing dominance in the next phase of automotive expansion.

Broader Asia Pacific markets, including India, Japan, and South Korea, continued gaining long-term strategic importance as rising incomes, industrialization, manufacturing investment, and battery supply-chain expansion accelerated regional vehicle adoption.

Mature markets in Europe and North America are experiencing slower structural growth due to market saturation, economic pressure, and longer replacement cycles.

As a result, the future competitive landscape may be determined not only by where vehicles are sold, but by which regions can scale electrification most affordably and efficiently.

2. Chinese Automakers and Affordable NEVs Are Driving the Next Growth Wave

While legacy automakers such as Toyota, Volkswagen Group, Hyundai-Kia, GM, and Ford still dominate total global vehicle volume, the composition of industry growth is rapidly changing.

Chinese automakers are leading the fastest-growing segments of the global NEV market, particularly affordable EVs and plug-in hybrids aimed at mass-market consumers.

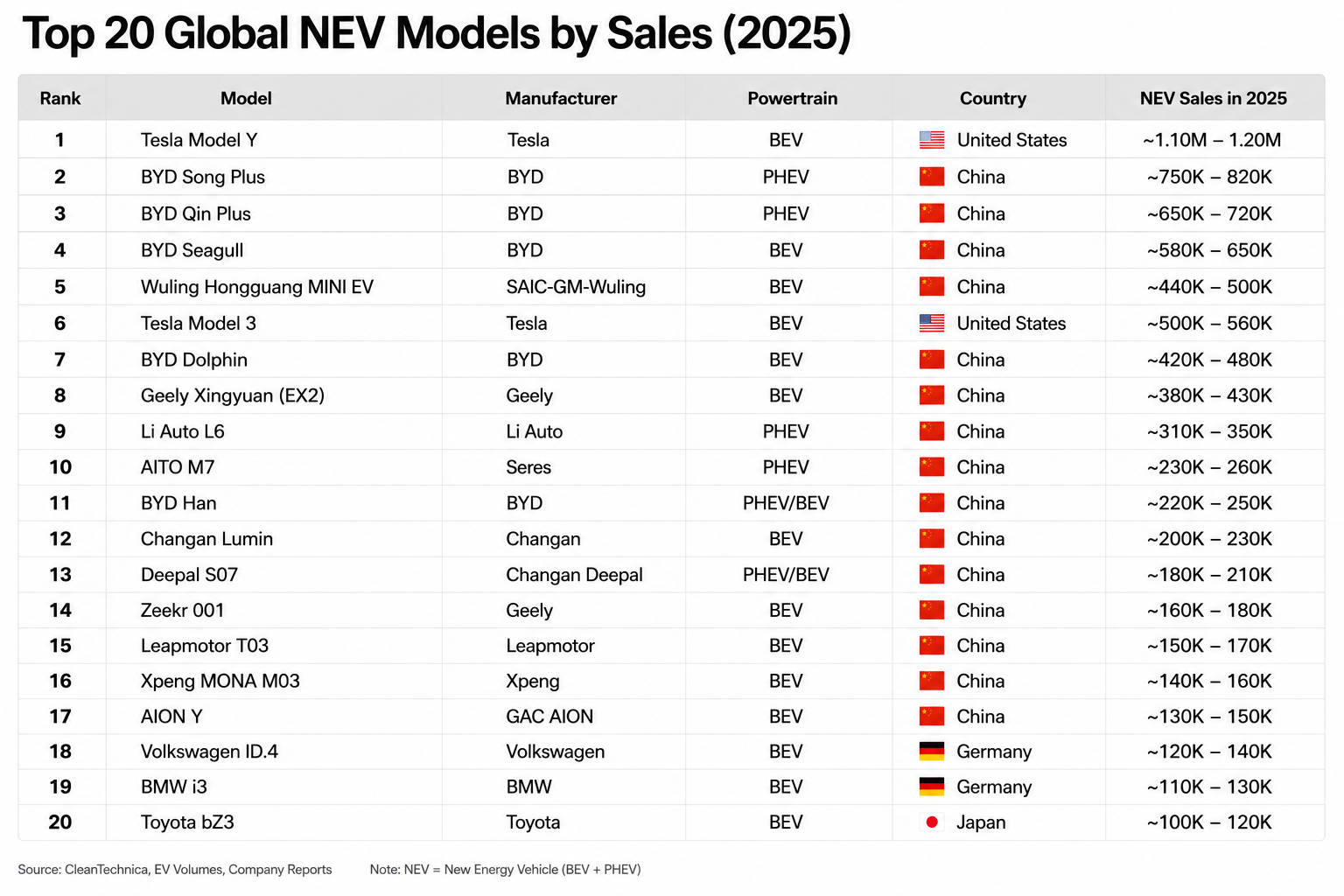

BYD emerged as the world’s largest NEV manufacturer in 2025 with ~4 million plug-in vehicle sales, over 950% growth since from 2020-2025, while companies such as Geely, SAIC, Changan, Chery, Leapmotor, and GAC continued expanding rapidly across both domestic and export markets.

Tesla’s Model Y and Model 3 remained global EV volume leaders, the broader Top 20 NEV rankings are filling up with lower-cost, high-volume vehicles such as the BYD Song Plus, BYD Qin Plus, BYD Seagull, and Wuling Hongguang Mini EV, signaling that EV adoption is moving into mainstream and price-sensitive consumer segments.

This shift is becoming especially visible across Southeast Asia, Latin America, the Middle East, and other emerging markets, where lower vehicle costs, easier financing, reduced day-to-day transportation expenses, and practical charging access may matter more to consumers than advanced software features or autonomous-driving technology.

Chinese automakers are benefiting from several structural advantages:

- Lower production costs

- Strong battery and supply-chain positioning

- Faster product development timelines

- Highly competitive vehicle pricing

- Wide EV and hybrid model ranges

- Rapid expansion of overseas retail and distribution networks

As a result, Chinese automakers appear relatively well positioned due to scale, supply-chain integration, and cost competitiveness.

This scale is highlighted in the strength of Chinese NEV exports in 2026, which have moved from being a regional growth story to a global competitive force. In 2025, China exported roughly 2.6 million electric and plug-in hybrid vehicles, approximately double the prior year. By the first quarter of 2026, Chinese NEV exports had already reached 950,000 units, more than doubling year-on-year, with March alone setting a new monthly high of around 371,000 units.

Of these Chinese exports, BYD has shipped over 450,000 from January to April 2026, and is on target to meet it's expectations of 1.4-1.5m global shipments.

If current export and domestic demand trends continue, BYD could potentially approach 5–6 million annual vehicle sales in 2026, placing the company among the world’s largest automaker groups by volume.

3. Fuel Prices and Consumer Economics Accelerated EV Interest in 2026

Early 2026 became an important behavioral inflection point for the global automotive industry, as renewed geopolitical tensions involving Iran, Israel, and the United States contributed to rising oil-market volatility and elevated concern around fuel security across many fuel-import-dependent economies.

The March 2026 Top 20 global NEV rankings highlighted several major industry trends simultaneously:

- Tesla Model Y remained the world’s highest-volume EV model

- BYD continued dominating global PHEV scale

- Chinese manufacturers occupied a majority of Top 20 NEV rankings

- Affordable EVs and PHEVs drove industry growth

- EV adoption expanded beyond early adopters into mass-market consumers

Consumer Response During Fuel-Price Volatility in the Philippines

In March 2026 in the Philippines, DOE retail fuel monitoring showed gasoline prices in some areas approaching ₱129/L during peak volatility periods.

The price surge coincided with a noticeable shift in consumer behavior across the automotive market. Buyers increasingly prioritized fuel efficiency, operating-cost stability, financing affordability, and reduced gasoline dependence when evaluating vehicles.

AutoDeal platform inquiry data between February and April 2026 reflected this shift, with growing consumer interest in EVs, hybrids, and plug-in hybrids, particularly among mainstream buyers focused on day-to-day transportation economics.

For many consumers in Southeast Asia and other fuel-import-dependent economies, electrification is increasingly becoming an economic decision as much as a technological one.

AutoDeal NEV inquiries Surge +188%

The shift in consumer interest between February and April 2026 was significant, with AutoDeal inquiry data for EVs and plug-in hybrids rising 188% over the three-month period.

In February 2026, BYD was the only EV-focused brand appearing in the Top 10 most-inquired brands on the platform. By April, 7 of the Top 10 brands were EV or PHEV manufacturers, the majority of them Chinese automakers.

The surge reflected a rapid shift in consumer priorities during the period of fuel-price volatility. Buyers increasingly focused on reducing monthly fuel expenses, improving day-to-day operating costs, and finding alternatives to gasoline dependence.

If elevated fuel prices and economic uncertainty persist, momentum toward hybrids, plug-in hybrids, and EVs may continue accelerating across price-sensitive Southeast Asian markets through the remainder of 2026.

4. The Future of NEV Growth Through 2030

Global vehicle sales are expected to continue expanding through 2030, potentially surpassing 110–115 million annually and NEV penetration is expected to continue rising rapidly, with many industry projections now suggest NEVs could account for approximately 45–55% of global passenger vehicle sales by 2030.

The EV Transition Will Likely Move at Different Speeds Across Regions

The global shift toward electrification is increasingly being shaped not only by technology, but also by energy security, industrial policy, manufacturing scale, and consumer economics.

China currently holds major structural advantages across battery production, critical mineral processing, vertically integrated supply chains, and lower-cost EV manufacturing, positioning its automakers strongly for the next phase of mass-market electrification. At the same time, many fuel-import-dependent regions across Southeast Asia, South Asia, Africa, and Latin America are seeking to reduce long-term exposure to oil-price volatility through gradual vehicle electrification.

Yet the transition remains uneven. In many developing markets, charging infrastructure, grid readiness, financing accessibility, and household purchasing power continue limiting the pace of adoption. As a result, hybrids and plug-in hybrids may remain important transitional technologies for longer than many earlier forecasts anticipated.

Several structural challenges could continue reshaping the pace of electrification across regions:

- Infrastructure Gaps: Charging bottlenecks and grid-capacity limitations remain major barriers to mass-market EV adoption outside urban centers.

- Supply-Chain Sovereignty: Competition for critical minerals, battery localization, and recycling capacity is becoming increasingly strategic for governments and manufacturers alike.

- Economic Friction: Affordability ceilings, financing constraints, and the gradual rollback of EV subsidies may slow adoption unless manufacturers achieve stronger cost parity with internal combustion vehicles.

Moving forward, competition may increasingly center on affordable ownership, localized production, battery recycling, supply-chain resilience, and lower-cost vehicle platforms rather than premium positioning alone.

Rather than following a single synchronized pathway, the global EV transition may ultimately unfold as a multi-speed transformation shaped by regional economics, infrastructure readiness, and consumer practicality.

Sources & References

This article incorporates data, estimates, and analysis synthesized from:

- OICA

- MarkLines

- EV Volumes

- JATO Dynamics

- BloombergNEF

- McKinsey Mobility

- LMC Automotive

- Counterpoint Research

- Company investor filings and annual reports

- Philippine DOE fuel-price monitoring

- AutoDeal platform inquiry and lead data

- China Passenger Car Association (CPCA)

- China Association of Automobile Manufacturers (CAAM)

- BYD investor disclosures and monthly sales reports

- Geely Automobile Holdings monthly sales disclosures

- SAIC Motor sales reports

- Customs and trade-export tracking data

- Reuters automotive industry reporting

- CleanTechnica EV market tracking

- Rho Motion EV research

Certain forecasts and visualizations represent synthesized industry estimates intended for illustrative analytical purposes.